On the 19th of May 2026, Hyundai Motor Group quietly published a press note saying it plans to deploy more than 25,000 Atlas humanoid robots across its Hyundai and Kia plants, with U.S. production scaling by 2028. It is the single largest humanoid order on record, and most of the trade press buried it under the rolling China-vs-US AI infrastructure story. If you missed it, you missed the moment humanoid robots became tangible as an industry.

I wrote earlier this year about growing up with Tamagotchis, AIBO, and Johnny Five - a personal piece about why I find this whole field interesting in the first place. This is the grown-up version of that post. Humanoid robots are becoming a reality at scale. They are showing up in factories, signing enterprise deployment contracts, and running multi-year roadmaps with large corporations.

This post is a deeper look at the four platforms worth understanding right now, with honourable mentions and a view of which ones deserve your head-space. I’m not trying to be exhaustive - the list-ai-humanoid-robots index covers more than 50 platforms and humanoid.guide tracks 173 at the time of writing.

Table of contents

Open Table of contents

- How to read this post

- The industrial trio at a glance

- Atlas (Electric) - The Incumbent Capability Leader

- Figure 03 + Helix - The Vision-Language-Action Bet

- Optimus Gen 3 - The Vertical Integration Play

- Unitree H2 and R1 - The £13K Wildcard

- Honourable mentions

- Picking a winner is the wrong question

- The videos… you can’t unsee

- What I would actually buy (if I could afford to)

- Closing thought

How to read this post

Each robot has a spec card with two kinds of data. Raw numbers (height, weight, top speed, battery, payload) are sourced from manufacturer disclosures and the Notion list of commercial humanoid robots. The segmented bars are editorial 0-10 scores - my call about where each robot sits within the current humanoid field, not against an absolute scale. A speed score of 8 means “fast for a humanoid”, not “fast for a car”. The “Dexterity” score is the spiciest of these, because nobody has agreed how to measure it; treat it as a vibes check from someone who has spent too long watching robot demo reels.

The industrial trio at a glance

Atlas (Electric)

Boston Dynamics · USA

Figure 03

Figure AI · USA

Optimus Gen 3

Tesla · USAAtlas (Electric)

Boston Dynamics · USAFigure 03

Figure AI · USAOptimus Gen 3

Tesla · USAThese three are the platforms most likely to be in a factory near you within the next 24 months. They compete for the same enterprise pilots, the same Tier-1 automotive contracts, the same logistics deployments. Unitree H2 lives in its own section because its positioning - open hardware, research grade, consumer-priced sibling - doesn’t comparably stack against the industrial trio.

Atlas (Electric) - The Incumbent Capability Leader

Atlas (Electric)

Hydraulic ancestry, now silent. The incumbent capability leader, with Hyundai writing the biggest order ever placed for a humanoid.

Atlas (Electric)

Hydraulic ancestry, now silent. The incumbent capability leader, with Hyundai writing the biggest order ever placed for a humanoid.

Boston Dynamics retired the hydraulic Atlas in 2024 and replaced it with an all-electric platform that looks, frankly, slightly uncanny. The 360-degree joint rotation is the headline feature: Atlas can do things human bodies physically can’t. Joints that rotate a full 360 degrees let it reach, twist, and recover in ways that look wrong until you realise they’re better.

The technical story is well-rehearsed: decades of mobility research, fluid recovery from falls, gait control good enough that it can pick its way across construction-site rubble without falling over. None of that is news. What is news is the commercial story, which until April 2024 was essentially “Boston Dynamics shows another video, social media reacts, no robots ship”.

That changed with the Hyundai announcement. Hyundai Motor Group owns Boston Dynamics outright, which means Atlas now has a guaranteed deployment customer at scale. 25,000 units across Hyundai and Kia plants is the kind of number that lets the manufacturing function actually plan capacity, which is the precondition for unit economics that don’t look ridiculous on a cap table.

Where Atlas struggles - and the spec card reflects this honestly - is battery life. A one-hour active runtime is a real operational constraint. Factory floors get around this with swap stations and choreographed downtime, but it means Atlas is not a roving worker; it’s a stationed specialist that does specific tasks within a known cell. That’s a perfectly reasonable architecture, but it’s worth being clear-eyed about. Atlas is not going to walk around a warehouse picking orders for eight hours.

The other thing worth saying: Boston Dynamics is one of the few platforms where the robot is the brand, not the AI stack. Their model layer is impressive but not as marketed as Figure’s Helix or Nvidia’s GR00T. If you want a Boston Dynamics-shaped opinion on embodied AI strategy, you have to read between the lines of their behaviour-tree-plus-RL technical disclosures.

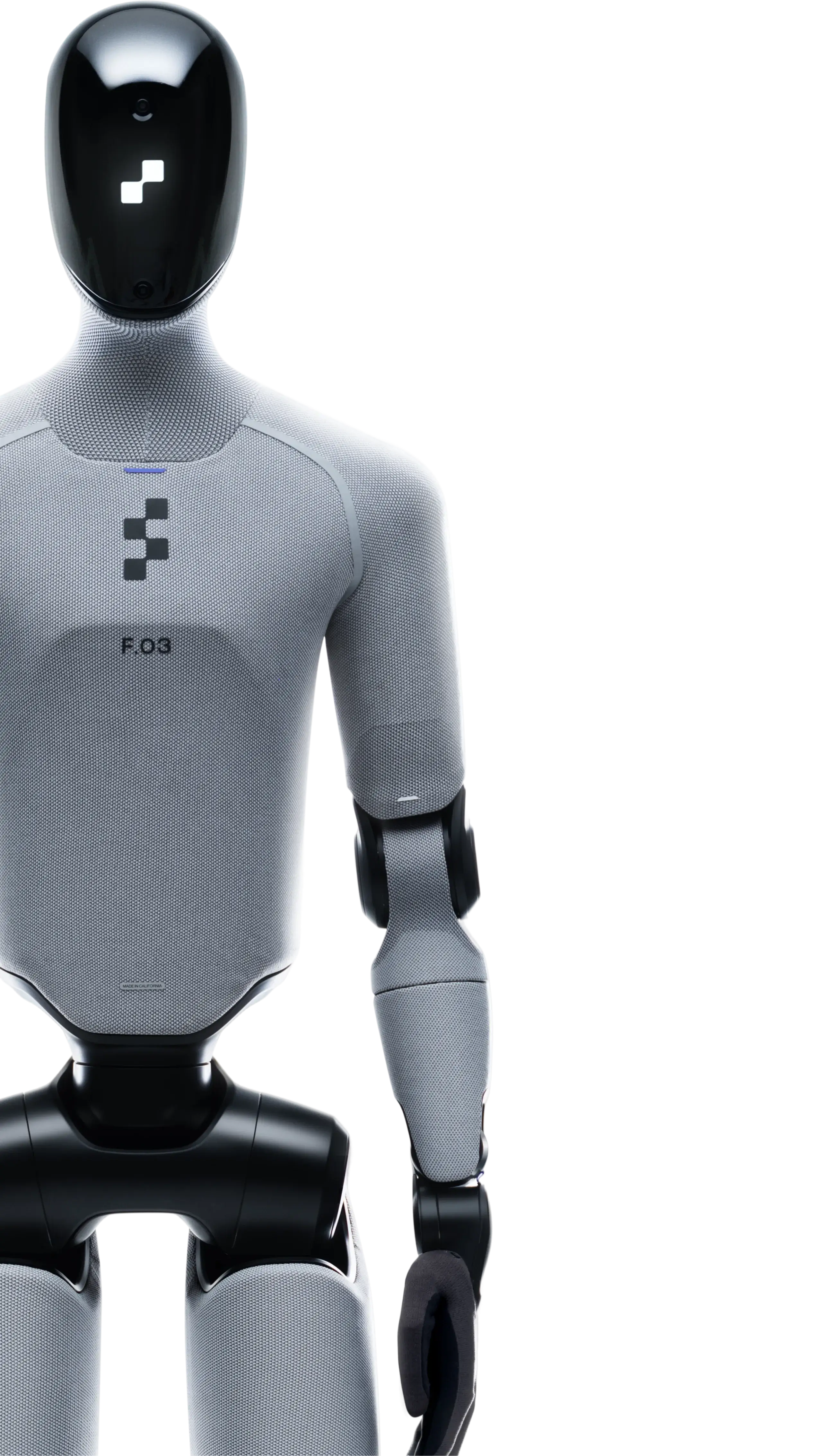

Figure 03 + Helix - The Vision-Language-Action Bet

© Figure AI

© Figure AIFigure 03

The vision-language-action bet. Helix runs on board, BMW lines run in production, and Figure thinks the model layer wins long-term.

© Figure AIFigure 03

The vision-language-action bet. Helix runs on board, BMW lines run in production, and Figure thinks the model layer wins long-term.

Figure AI is the platform that has bet hardest on the AI model layer being where the value accrues. The hardware is competent. The differentiator is Helix, Figure’s in-house vision-language-action model that runs on board and lets the robot accept natural-language tasking the way you’d brief a junior on their first day.

The BMW pilot is the proof point. Figure 02 was on BMW production lines in 2025 doing chassis sheet-metal work; Figure 03 is the iteration that expands the role and tightens the integration. This is one of the few cases where you can point at an actual factory and say “yes, the humanoid is doing the job”, not “the humanoid did the job once in a demo”.

Helix matters because of what it’s not. It is not a task-specific behaviour tree. It is not a hand-engineered grasping policy. It is a learned model that maps language and vision directly to motor commands, in the same conceptual lineage as language models that map tokens to next-tokens. Figure’s strategic bet is that as Helix improves, the same robot does more jobs, which is a fundamentally different unit economics story than the per-task-engineering model the industry started with.

If that bet pays off, Figure becomes the obvious enterprise default for general-purpose humanoid work. If it doesn’t - if VLA models plateau, or if on-device inference can’t keep up with the latency budget for safety-critical tasks - Figure ends up as a competent industrial humanoid in a crowded market.

Optimus Gen 3 - The Vertical Integration Play

Optimus Gen 3

Vertical integration as competitive moat. FSD-derived compute, in-house actuators, a £16K ($20K) consumer narrative that the rest of the industry rolls its eyes at.

Optimus Gen 3

Vertical integration as competitive moat. FSD-derived compute, in-house actuators, a £16K ($20K) consumer narrative that the rest of the industry rolls its eyes at.

Tesla announced Optimus Gen 3 at the start of 2026, and the announcement was - and I am being generous here - underspecified. The hardware shown was an iteration on Gen 2 with refined actuators, a cleaner head module, and improved hands. The pitch was the same as it’s been since 2021: this is the consumer humanoid, this is going to be priced like a small car, this is going to live in your house in a few years.

I have a lot of time for Tesla’s engineering teams. I have considerably less time for Tesla’s timelines. Every announced delivery date for Optimus has slipped, and the gap between the rendered concept videos and the production reality remains larger than the company would like you to notice.

That said, the strategic position is genuinely strong. Tesla has three things very few other humanoid companies have:

- In-house silicon and a training stack. The same Dojo and FSD machinery that trains autonomous driving policies can train robot policies. That’s a meaningful structural advantage.

- A manufacturing function that knows how to scale. If Optimus Gen 3 ships, Tesla can produce it at volumes that most pure-play humanoid companies cannot. The supply chain learnings from the Model 3 ramp matter here.

- An installed compute base. FSD-derived neural nets running on Tesla’s in-house silicon means Tesla owns the latency budget end-to-end. No NVIDIA dependency, no cloud roundtrip.

Optimus Gen 3 is a strong long-term contender that has not yet proven it can ship. If you’re following this space and trying to separate signal from noise, do not let the Tesla brand carry the conversation. Press releases and deployed unit counts are not the same thing, and right now Tesla has plenty of the former and none of the latter.

Unitree H2 and R1 - The £13K Wildcard

Unitree H2

The Hangzhou wildcard. Research-grade flagship priced like a sensible car, and the R1 sibling lands at £13K ($16K) - which changes who can play.

Unitree H2

The Hangzhou wildcard. Research-grade flagship priced like a sensible car, and the R1 sibling lands at £13K ($16K) - which changes who can play.

Unitree is the platform that quietly changed the conversation about who gets to do humanoid robotics. The H2 is a competent research-grade flagship at roughly £55K ($70K) - a fraction of Atlas-class platforms, but still firmly in “your university lab can buy one” territory. The R1, Unitree’s consumer-priced sibling at around £13K ($16K), is the more important product.

£13K ($16K) is the price point at which independent researchers, mid-sized engineering teams, and well-funded hobbyists can put a humanoid in front of their actual problem space. That changes the demographics of the field. The companies that have spent ten years building proprietary humanoid platforms are competing against an open-hardware-ish, ROS 2-native ecosystem that has thousands of researchers iterating on it for free.

If you’ve watched the Unitree demo reel and assumed the kung-fu sequences and acrobatic recoveries are cherry-picked - they are, of course, but the underlying gait control is genuinely strong. Top speed of 3.3 m/s is the fastest in the field. Battery life and payload are weaker than the industrial-class platforms, which reflects the platform’s positioning: this is not a factory robot, it is a research robot you can iterate on.

The strategic question is whether Unitree (and the broader Chinese humanoid sector - AgiBot, Xpeng, UBTECH, Engine AI) becomes the Android of humanoid robotics: the open, accessible, lower-cost ecosystem that ends up running on more units than the premium platforms. CNBC’s recent reporting on China positioning humanoids for the workforce suggests that this is not an accident; it is policy.

The GD01 - Unitree’s Mecha Moment

GD01 Mecha

The world's first production-ready manned mecha. Half a ton of bipedal machine with a cockpit, a transformation mode, and a price tag that says 'we're serious'.

GD01 Mecha

The world's first production-ready manned mecha. Half a ton of bipedal machine with a cockpit, a transformation mode, and a price tag that says 'we're serious'.

And then, on 13 May 2026, Unitree unveiled the GD01: what they claim is the world’s first production-ready manned mecha.

This is not a humanoid robot. This is a half-ton bipedal machine with a cockpit. Founder Wang Xingxing personally piloted the GD01 in the demo video, walking it through terrain, transforming between bipedal and quadruped modes, and - because this is Unitree - smashing through a brick wall for good measure.

At £475K ($600K) this is not a consumer product. It is a statement of engineering ambition and a positioning play. Unitree is saying: we can build at every scale, from the £13K ($16K) R1 to a manned walking vehicle that weighs as much as a horse. The underlying gait control, actuator design, and structural engineering required to keep a half-ton biped stable with a human inside is a non-trivial demonstration of capability.

Commercially relevant in 2026? Probably not beyond very niche rescue and mining applications. But as an engineering flex that attracts talent, funding, and government attention in the Chinese robotics ecosystem, it does exactly what it needs to. The GD01 is Unitree’s way of saying the ceiling is a lot higher than research-grade humanoids - and they intend to build toward it.

Honourable mentions

The shortlist of platforms that didn’t make the headline four but absolutely belong in the conversation:

1X NEO Gamma - 1X Technologies, US/Norway. The domestic-focused humanoid with the soft tendon-driven exterior. NEO is the platform betting that the first mass-market humanoid lives in your house, not your factory. OpenAI was an early investor. The form factor (textile shell, low-noise actuators) prioritises being safe to share a room with over being fast or strong. Smart wedge into a different category.

Apptronik Apollo - US. Mercedes-Benz pilot deployments, GXO logistics work, Nvidia GR00T partnership. Apollo is the platform you’d describe as the Toyota of humanoids: not the fastest, not the showiest, but unfussy and deployable. If I had to bet on which industrial humanoid has the largest installed base in 2027, Apollo is genuinely my pick over Atlas.

Agility Digit - US. Amazon warehouse deployments are real and ongoing. Digit’s morphology is non-anthropomorphic from the knee down (the ostrich-leg comparison is unavoidable), which is an honest engineering choice rather than a fashion statement: it makes the gait simpler. Agility is older and more deployment-mature than half the platforms above.

Sanctuary AI Phoenix Gen 7 - Canada. The dexterity specialist. Phoenix’s hands are the best-rated in the field for fine manipulation, which makes Sanctuary the bet for tasks that don’t fit Atlas-style heavy lifting. They’ve been quieter on commercial deployment than the US players, but the technical work is serious.

NEURA Robotics 4NE-1 - Germany. The European entrant, with a “cognitive robot” framing that maps reasonably onto the Helix VLA story but with a European AI-act-aware governance model. Worth watching if you care about how EU regulation shapes embodied AI - 4NE-1 is being designed with the AI Act in mind from day one.

Xpeng Iron - China. The automotive crossover. Xpeng makes electric vehicles and decided humanoids were a logical adjacent product, which is the same playbook Tesla is running. Worth watching because the Chinese automotive supply chain is unmatched on cost.

AgiBot A2 / A2-W - China. The wheeled A2-W lists at £50K ($64K) on humanoid.guide and is the commercial-deployment platform that often gets ignored in Western coverage. AgiBot is doing real work in Chinese manufacturing and warehouse settings, and is one of the platforms most likely to undercut the US incumbents on price.

Picking a winner is the wrong question

The temptation in any comparison post is to declare a winner. I’m not going to, because the field has split into four distinct strategies that are not competing for the same outcome:

- Capability-first: Atlas. Win the hardest physical tasks, sell to customers who need that. Hyundai is buying because nobody else can do what Atlas does at that scale.

- Model-first: Figure (and to a lesser extent Apollo via the GR00T partnership). Win the AI layer, become the default substrate for general-purpose humanoid work.

- Integration-first: Optimus, Xpeng Iron. Own the stack end-to-end, ride down the cost curve via vertical manufacturing.

- Price-first: Unitree, AgiBot. Make humanoid robotics accessible enough that the ecosystem does the differentiating for you.

If you’re trying to understand which of these platforms is actually going to matter, map each one to these archetypes before anything else. If a company’s messaging doesn’t make it obvious which lane their platform is running in, that’s a tell.

The four archetypes also tell you which platforms are at risk. Capability-first leaders lose their edge when capability gets commoditised. Model-first leaders stall if VLA models plateau. Integrated stacks get undercut by good-enough modular components sold at half the price. And price-first ecosystems get squeezed when the premium platforms find their own cost curve. Each of these has happened in other technology categories; expect at least one to happen here.

The videos… you can’t unsee

Two videos dropped in the last few weeks that the spec cards and strategy analysis can’t quite capture.

The first: Boston Dynamics published a video on 18 May titled “Atlas, can you bring me a drink?” Atlas doesn’t bring a drink. It brings the entire fridge. The robot picks up a mini-fridge from a wooden block, carries it across the lab, adjusts its grip and posture mid-stride to compensate for the shifting weight, and sets it down on a table. The whole thing is trained via reinforcement learning - thousands of simulated variations of fridge weight, grip friction, and surface angle, distilled into a policy that generalises to the real object. It is technically beautiful. It is also a machine doing manual labour that looks exactly like a human doing manual labour, except it never clocks off.

The second: Figure AI ran a livestreamed 200-hour autonomous shift at their Sunnyvale headquarters, three Figure 03 robots - nicknamed Bob, Jim, and Rose by viewers who’d been watching the stream - sorting packages around the clock, processing nearly 250,000 of them without a single hardware failure. When the 200-hour mark hit, the team behind the workstation popped champagne. Robot Rose kept sorting, uninterrupted, while the celebration happened around her. That contrast is the thing that sticks. We were celebrating what, for a human, would be a brutal continuous work record - and the robot had no idea, and wouldn’t have cared, and was already reaching for the next package.

I grew up watching films where humanoid machines do the jobs humans don’t want to do. I, Robot. Ex Machina. Blade Runner. The framing in those films is always dual: we celebrate the ingenuity of the design, the engineering triumph of a machine that moves like us, and simultaneously feel uneasy about what it means when that machine is put to work. The unease lands on the system that deploys the robot and the humans whose labour it displaces, not on the machine itself.

We’re watching those films happen now, in fragments, on YouTube and Instagram. A robot carries a fridge. A robot works a ten-hour shift on a production line for five months straight. Amazon’s leaked internal documents describe plans to automate 75% of operations by 2033, potentially avoiding 600,000 new hires. A humanoid ran a half-marathon faster than any human in April. The individual clips are impressive. The aggregate picture is something else.

I don’t think this is inherently dystopian. Plenty of the work being automated is genuinely unpleasant - repetitive, physically demanding, injury-prone. If a robot can load sheet metal into a welding fixture for eleven months without developing a repetitive strain injury, that is a net good for the humans who would otherwise be doing it. The question is whether the economic value freed up by that automation flows to those displaced workers or exclusively to the shareholders who deployed the robot. History suggests the latter happens first and the former happens eventually, if at all, and only under political pressure.

The pace of improvement is the part that should genuinely astonish you. Figure 02 was a research curiosity in early 2024. By late 2024 it was on a production line. By 2025 it was running daily shifts. By early 2026 it had produced 30,000 cars and been retired in favour of a better model. That timeline - from lab to production to obsolescence - is about eighteen months. The next iteration will be faster. The one after that, faster still. The compound rate of improvement in embodied AI is tracking closer to software than to traditional industrial automation, and that is genuinely unprecedented for physical machines.

None of this means robots are coming for every job next year. It does mean that the gap between “impressive demo reel” and “deployed at scale on a production line” has collapsed from a decade to months. We are living through the period where humanoid robots cross from science fiction into industrial reality, and the timeline is compressing faster than almost anyone predicted even two years ago.

What I would actually buy (if I could afford to)

This is the section everyone argues with. Here goes:

For a hobbyist or independent researcher: Unitree R1. £13K ($16K) is the price at which you can justify the purchase against a meaningful project, and the open ROS 2 stack means the broader research community is iterating with you. If R1 is sold out or out of your region, the Pollen Robotics Reachy 2 is the next sensible step.

For a factory pilot: Apptronik Apollo or Agility Digit. Both have real deployment history with real industrial customers, both have credible support contracts, and both are at the stage where you can pilot them without the vendor treating you as a science experiment. Atlas is technically better and Figure has the more interesting AI story, but for a first factory deployment in 2026, Apollo and Digit are the lower-risk choices.

For anyone making a five-year bet on the field: Figure, with hedges. The bet is that the model layer wins, that Helix-style VLA scaling holds, and that Figure’s enterprise deployment moat keeps pace with the model improvements. If Helix plateaus and the field consolidates around vertical-integration economics, the integrated platforms (Optimus, Xpeng) become the ones to watch. Either way, the VLA-vs-vertical-integration question is the most interesting strategic fork in the industry right now.

For a domestic deployment in three to five years: 1X NEO Gamma. The bet here is that the first viable home humanoid is one that prioritises being safe to share a room with over being capable of heavy lifting. That’s a different design constraint, and 1X is the platform that has internalised it most explicitly.

For nostalgia value: just go back and watch Short Circuit 2. Number Five is still alive, and none of the robots above have caught up to him on personality.

Closing thought

The conversation has moved past capability. Every platform in this post can walk, lift, manipulate, and learn. The interesting question now is what we choose to do with that capability - and specifically, whether we build an industry that treats humanoid labour as something worth getting right, or one that sleepwalks into the dystopia we’ve been rehearsing in cinema for fifty years.

The sci-fi trope is always the same: we build machines in our image, we put them to work, we treat them as tools, and eventually they become aware enough to resent it. I, Robot. Blade Runner. Westworld. The narrative arc depends on mistreatment as the catalyst for singularity. It is a story about our worst instincts projected onto our best engineering.

I don’t think that’s the future we’re building toward - not because singularity is impossible, but because the framing is wrong. The robots sorting packages in Sunnyvale aren’t suffering. They aren’t going to wake up resentful. The ethical question isn’t “are we being cruel to the machine?” It’s “are we being careless with the humans the machine displaces, and are we building governance structures that keep pace with deployment?”

The version of the future I find more compelling - and more honest about why most of us are drawn to this field in the first place - is the one where humanoid robotics keeps advancing because we genuinely want to understand embodied intelligence. Not just to automate warehouse shifts, but to refine our models of locomotion, dexterity, perception, and decision-making into something more intricate and more complete than what we have today. Every VLA model that learns to generalise across tasks is also a piece of cognitive science. Every reinforcement-learning policy that teaches a robot to carry shifting weight is also a contribution to our understanding of how physical intelligence works.

The people building these platforms aren’t exclusively motivated by labour arbitrage. Many of them got into robotics the same way I got into it - watching Johnny Five, reading Asimov, building LEGO Technic mechanisms on a bedroom floor and wondering whether something that moves like a living thing could eventually think like one. That curiosity is worth protecting. The best version of this industry is one that stays close to it: advancing capability not just because it is commercially useful, but because humanoid robotics is one of the most interesting engineering problems humans have ever set themselves, and the models we build along the way teach us something about ourselves.

The ethical deployment question and the scientific curiosity question aren’t in tension. They’re the same question asked at different altitudes. Build the governance. Protect displaced workers. And keep pushing the boundary of what these machines can do, because the understanding we gain from that work is worth having regardless of which platform wins the enterprise contract.

Further reading and sources

- Awesome List of AI Humanoid Robots (jk4e) - the most useful index of the field

- humanoid.guide - comprehensive specs and industry news

- List of Commercial Humanoid Robots (Notion) - tracks commercially available platforms

- Boston Dynamics Atlas, Figure AI, Tesla Optimus, Unitree Robotics - manufacturer sources